- Bachoco is a value stock, trading under book value and with a P/E ratio of just under 12x.

- The Balance Sheet is as strong as it gets, it currently has nearly $800 million in cash and a market capitalization of $1.813 Billion.

- The Management’s intention to grow through acquisitions in the Mexican market, supported by its low debt levels, gives it a very positive outlook.

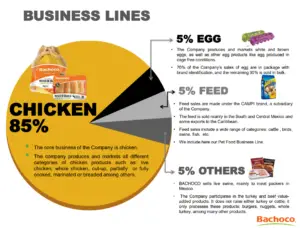

Industrias Bachoco, S.A.B. de C.V. (NYSE: IBA), is the leading Mexican poultry producer and is among the ten largest worldwide. The company’s operations are focused on chicken, but it also offers feed, turkey, swine, and beef. It has been able to gain some market share in the competitive U.S. market and it should strengthen its position going forward. In the past decade, it has been able to achieve a solid increase in sales and income per share, which should continue in the long term. The company just acquired a controlling stake in Sonora Agropecuaria S.A. de C.V. (SASA), a swine producer and processor in Mexico. The management continues with its plan to grow through acquisitions. At the same time, it is diversifying its business lines and reducing exposure to the poultry market. Thus, the acquisition will allow Bachoco to penetrate into different markets and solidify the company’s position.

Source: Investor Presentation

Market Overview

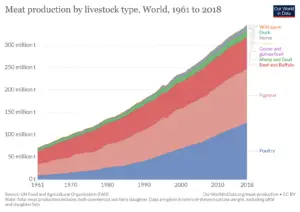

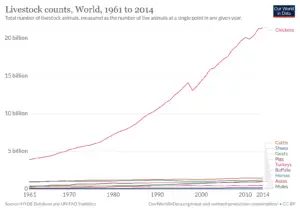

Over the course of the second half of the 20th century and into the 21st century, the trend has been clear: the type of livestock production that has grown the most has been poultry. This trend should continue in this century, given the relatively low cost of breeding chickens and its nutritional value.

Source: Our World in Data

Source: Our World in Data

On a large scale, poultry remains one of the few types of livestock that we were able to mass-produce and scale effectively. Besides that, it remains the cheapest option when accounting for the resources used to produce animal protein. In 2019, the global poultry market grew by 6%, with China being the largest consumer, with a consumption of around 20 million tonnes annually, and the U.S. comes in second, at 19 million tonnes.

Source: Our World in Data

Source: Our World in Data

In late 2019, due to pig shortages, China was forced to lift the ban on U.S. poultry imports, which was in place for more than 4 years. Despite the fact that the ban was lifted, Chinese poultry production is increasing at a fast pace, reducing the need for imports. China remains an interesting market, with a lot of growth prospects, and Bachoco could, in time, ponder to enter this market. Also, despite the pandemic, Brazil has been able to keep the production at a normal rate and was able to increase its Chinese exports.

Pandemic impact in poultry and Bachoco

Due to COVID-19 and the halted production of poultry in China, imports have surged 76% compared to the same period in 2019. This was mainly driven by the higher pork prices during this period, with consumers turning to chicken as a cheaper alternative to pork.

Since the company has most of its operations in Mexico and the production costs tend to be lower than in the U.S., it has been able to increase its market share over time. The competitors have been offering more value-added products, which has led them to capture higher margins than Bachoco. With high unemployment rates in the U.S. and with consumers saving more, a shift towards chicken as a cheap protein source positively impacts Bachoco’s operations.

Source: Investor Presentation

Source: Investor Presentation

Bachoco's Management

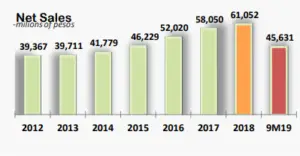

Management remains focused on its growth through acquisition plans and should reduce the dependence on poultry as a main source of revenue going forward. The recent pandemic affected Mexican poultry producers and is the reason the company missed the earnings estimates in the last quarter. For the first half of the year, net sales were up by 3% YoY and the net income increased 13% YoY. Despite the challenges in the short term, the situation gives Bachoco the ability to capture even more market share in Mexico. Given the company’s strong balance sheet and management’s intention of growing through acquisitions, growth is expected in the near future.

Acquisitions

The Mexican Antitrust Authorities approved Bachoco’s acquisition of a controlling stake of 54.8% in Sonora Agropecuaria S.A. de C.V. (SASA). SASA is involved in swine processing and distribution in Mexico. The acquisition allows Bachoco to further diversify its revenue streams, boosting its existing swine plants to work at full capacity. In the past, due to low production, the company was forced to buy swine in the open market. The management wants to export most of the product to countries, such as Japan, China, and the U.S. Bachoco is looking for further acquisitions in the local Mexican market to solidify its market position. When asked about it in the last earnings call, the management reiterated the intention of having debt under 2.5x EBITDA.

Bachoco Valuation

The stock remains undervalued despite the positive outlook on the company. It trades at a price/sales ratio under 0.7, and under Book value, despite having been able to increase book value per share in the past. Thus, it is clear that the stock offers a margin of safety and interesting return prospects for long-term investors. Even though it has a P/E ratio under 12x, it is still growing its sales at a decent pace, and its earnings should continue to rise in the future.

Source: Investor Presentation

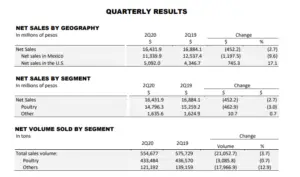

The balance sheet remains one of Bachoco’s strong points, with low debt, and a cash pile ready to deploy to further increase its growth prospects. The debt to equity ratio remains around 0.06 and the current ratio is nearly 4. The company has been paying a regular dividend since 2015 and the management likes to keep the payout ratio under 25%. Therefore, it allowed Bachoco to grow its cash pile over the years, which can now be deployed to make acquisitions. Given the value proposition the stock offers, Zacks Equity Research attributed the stock a Zacks Rank of #2 (Buy) and an A for Value. For the second quarter, the company has managed to increase its U.S. sales by 17.1%. At the end of the second quarter, the U.S. represented 31% of the total sales.

Source: Second Quarter Results

Bachoco's Competition

The U.S. poultry market is dominated by 3 names who together have nearly 60% of the market share. Those are Tyson Foods (NYSE: TSN), Pilgrim's Pride Corp (NASDAQ: PPC), and Sanderson Farms Inc (NASDAQ: SAFM). On the Mexican market, Bachoco’s number one competitor is JBS (OTC: JBSAY).

| Bachoco | Tyson | Pilgrim's | Sanderson Farms | JBS | |

| Price/Earnings | 12.41 | 11.61 | 22.73 | N/A | 232.56 |

| Forward Price/Earnings | N/A | 9.62 | 9.12 | 33.9 | 9.24 |

| Price/Book | 0.9 | 1.41 | 1.72 | 2.06 | 1.54 |

| Price/Sales | 0.6 | 0.5 | 0.35 | 0.81 | 0.24 |

| Price/Cash Flow | 7.41 | 5.73 | 6.61 | 16.7 | 2.72 |

| Enterprise Value/EBITDA | 4.27 | 7.93 | 8.89 | 44.12 | 7.8 |

| Debt to Equity | 0.06 | 0.81 | 1.24 | 0.1 | 2.3 |

| Net Margin % | 4.85% | 4.26% | 1.55% | -0.63% | 0.10% |

| Return on Equity % | 7.61% | 12.62% | 7.88% | -1.56% | 0.74% |

| Dividend | 1.87% | 2.91% | N/A | 1.35% | 2.54% |

| Payout Ratio | 24.10% | 32.90% | N/A | 82% | 553.10% |

Source: Morningstar

When compared with competitors, Bachoco stands out as the cheapest business. Due to the lack of debt and its cash position assuring investors that they are getting value for the price they pay. Not only that, but Bachoco presents the best net margin. Compared to its peers, Bachoco is clearly a value stock trading at these levels.

Conclusion

Bachoco stands out as a well-run business in a defensive sector, trading at a low valuation making it a value stock. The company’s prospects remain positive and the management’s inorganic growth strategy will be able to increase its returns for investors over the long term. While diversifying the revenue streams through acquisitions, the company should be able to penetrate into new markets going forward.

Despite not being a high-growth sector, the poultry business has seen some growth in recent years. China remains an unexplored market for the company, and it shows that Bachoco still has some room to grow its business outside of the markets it already operates in. The pandemic has affected supply and demand within the industry and this may present opportunities for acquisitions. Bachoco operates in a recession-proof sector, and the stock presents a very limited downside while having a solid margin of safety. On the other hand, inflation will not negatively impact the poultry producer, since the potential higher costs it may incur could easily be passed directly to the consumer. Given the book value and the future prospects this is a value stock, that has a margin of safety of $37 per share.

We are long IBA. Read our disclosure.