- A small player in the growing PPE market.

- A strong balance sheet with supply chain control.

- ~25% of its market cap in cash, and no debt.

- Total liabilities of ~$17M covered by $21.7M in accounts receivable.

- Price-to-earnings of 6.8 when deducting COVID-19 related earnings and cash.

- Although pandemic-driven sales have boosted earnings the long-term outlook for the company and the sector remains positive.

Lakeland Industries (NASDAQ: LAKE) is a leading manufacturer of PPE (Personal Protective Equipment). LAKE’s customers include well-known companies like Chevron (NYSE: CVX), Heinz (NASDAQ: KHC), Shell (NYSE: RDS-A), Honeywell (NASDAQ: HON), Dow (NYSE: DOW). It even works with government entities such as the Department of Agriculture and the Department of Defense.

There are numerous companies that have benefited due to COVID-19, LAKE is one of them. It added over 500 new customers both distributors and end-users globally, generating over $12M in sales. Management is confident that 80% of these new customers will result in future sales post-COVID-19.

Demand for its disposable garments has risen, and it was able to boost margins and increase profitability. With the vaccine rollout, there are many investors doubting Lakeland Industries’ results will remain the same. Since 30% to 35% of Lakeland Industries’ sales are COVID-19-related.

Despite that, LAKE is well-positioned with manufacturing facilities in several emerging countries and a worldwide sales presence. Although LAKE works with some distributors it has for the most part control over its supply chain and this allows for higher margins. It is also developing new products such as cleanroom suits for the pharmaceuticals industry.

Market Overview

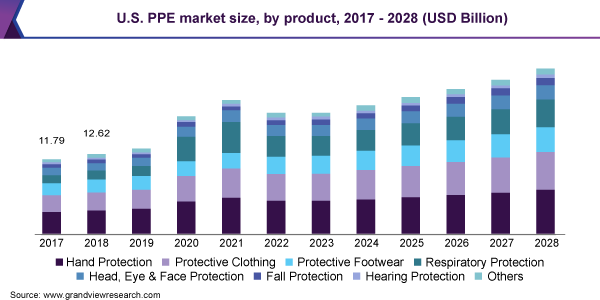

The global PPE market grew by ~153% from 2019 to 2020. Although some industry analysts are expecting a contraction somewhere in 2022 through 2023 the market will surely continue to grow globally and be driven in part by the US. The global PPE market is expected to reach $123.38B by 2027 at a CAGR of 9.6%.

About 44% of LAKE’s revenue is domestic and international sales account for 56%.

Lakeland Industries Short Interest

The fact that LAKE benefited from COVID-19 has led some investors to short Lakeland Industries expecting a contraction in margins and lower net income. Around 7.4% of the shares outstanding are shorted. Although ~35% of sales are attributed to COVID-19, the industrial demand for Lakeland Industries' products is there and it will not go away.

FY20 Results

LAKE grew revenues and earnings modestly from 2017 to 2019. LAKE has been beating analyst estimates over the last four quarters by a considerable amount.

Over the last year, the demand was such that LAKE’s personnel grew by 10%. Driven mostly by an increased international sales of 70%, the US segment lagged increasing only 26%. Overall revenues increased by 47.4% to $159M.

It was able to increase prices resulting in higher gross margins of ~49% compared with 35.2% in the previous year, which boosted net income by ~970% compared with 2019 to ~$35.1M. Diluted EPS came in at $4.31, generating ~$39M in free cash flow

Valuing Lakeland Industries

LAKE has a current market cap of ~$206M, with no debt. It currently holds $52.6M in cash, it should also be noted that it has ~$21.7M in accounts receivable and ~$49M in inventories, with just ~$17M in total liabilities. It is currently trading under 2x working capital with an Enterprise Value/EBITDA of ~3.4.

If we take into account last year's EPS of $4.31, the stock has a current price-to-earnings of just under 6. Since LAKE has no debt and it holds ~$6.6 in cash per share if we account for that the price-to-earnings is ~4.5.

Management estimates that COVID-19 related revenue is at most 35%. If we deduct 35% from last year’s earnings we arrive at an EPS of $2.8. If we deduct LAKE’s cash position to estimate the price-to-earnings without COVID-19-related sales we still arrive at a price-to-earnings of ~6.8.

Given the strong balance sheet and stellar performance in 2020, even if earnings decline significantly the stock is still fairly undervalued and has upside in the short-term and long term. For ~$25.74 a share you are getting $6.6 in cash plus and worst-case scenario earnings should be above $3 in 2021.

Possible Acquisition Target

Given the relatively small size of LAKE, and given that the competitive landscape includes large companies such as 3M (NYSE: MMM), Dupont (NYSE: DD), and Honeywell (NASDAQ: HON). It is likely that the company might be acquired especially given its current valuation. At the current valuation, current shareholders will certainly receive a considerable premium.

Final View

LAKE was a clear beneficiary of the pandemic. Despite the momentary increase in both the bottom line and top line, we think the stock is considerably cheap even if metrics deteriorate. The long-term outlook is positive for the PPE market overall, and LAKE is a well-established player in the industry despite its relatively small size.

It should also be noted that management might consider paying a dividend, depending on the results in 2021. The expected decrease in COVID-19-related revenue has attracted some short-sellers, but the company is clearly undervalued. Under $30, the stock is worth considering.

We have no position in any of the stocks mentioned. Read our disclosure.

Featured image source: LAKE